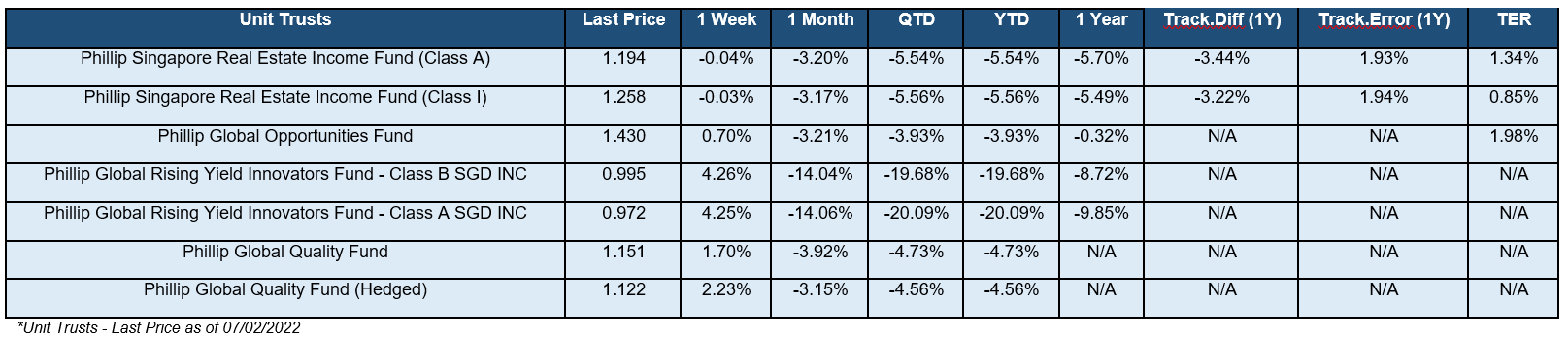

Weekly Commentary: 07 February 2022 – 13 February 2022

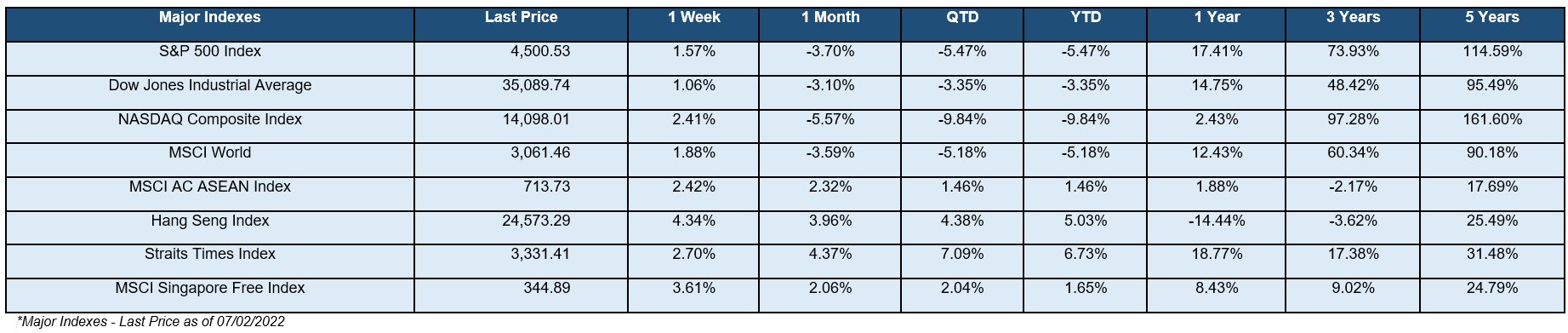

The stock market remained volatile last week but recorded overall gains for the second consecutive week. Value stocks as loosely represented by the DJIA (1.06%) improved slightly while the S&P 500 (1.57%) and the NASDAQ Composite (2.41%) recovered the most from the previous week. The STI (+2.7%) and Hang Seng (+4.34%), however, managed to advance its recovery from the week earlier.

The stock market remained volatile last week but recorded overall gains for the second consecutive week. Value stocks as loosely represented by the DJIA (1.06%) improved slightly while the S&P 500 (1.57%) and the NASDAQ Composite (2.41%) recovered the most from the previous week. The STI (+2.7%) and Hang Seng (+4.34%), however, managed to advance its recovery from the week earlier.

The Consumer Price Index published monthly by the U.S. Bureau of Labor Statistics (BLS) indicated that the inflation rate by the end of December has increased by 0.2% to reach 7%, the highest since 1982 and will likely remain in the high range in the near term due to the global energy crunch and supply chain disruptions. The average US inflation rate for 2021 was 4.7%, the highest since 1990. Rising inflation usually demand an increase in interest rate. This has been suppressed to stimulate economic growth in the past year, but the trend is most likely to be imminent this year due to the non-transitory high inflation and will inevitably punish the generously valued stocks.

The yield-curve has been flattening over the last few months. Two-year U.S. Treasury yields, which track short-term interest-rate expectations, have risen to 1.16% from 0.73% at the end of last year – a 60% increase. U.S. benchmark 10-year yields have gone up to about 1.8% from 1.5%, a 20% rise.

This week, the CBOE Volatility Index (VIX) closed 16% down from the previous week at 23.22 points. In the past month, the VIX reached a high of 38.94 points and a low of 16.58 points.

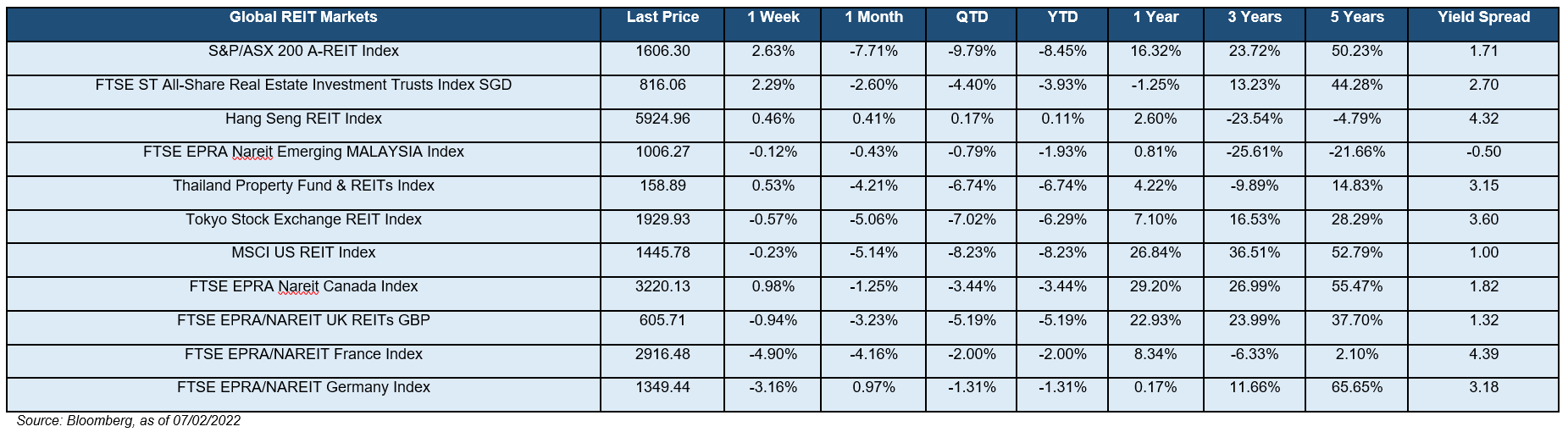

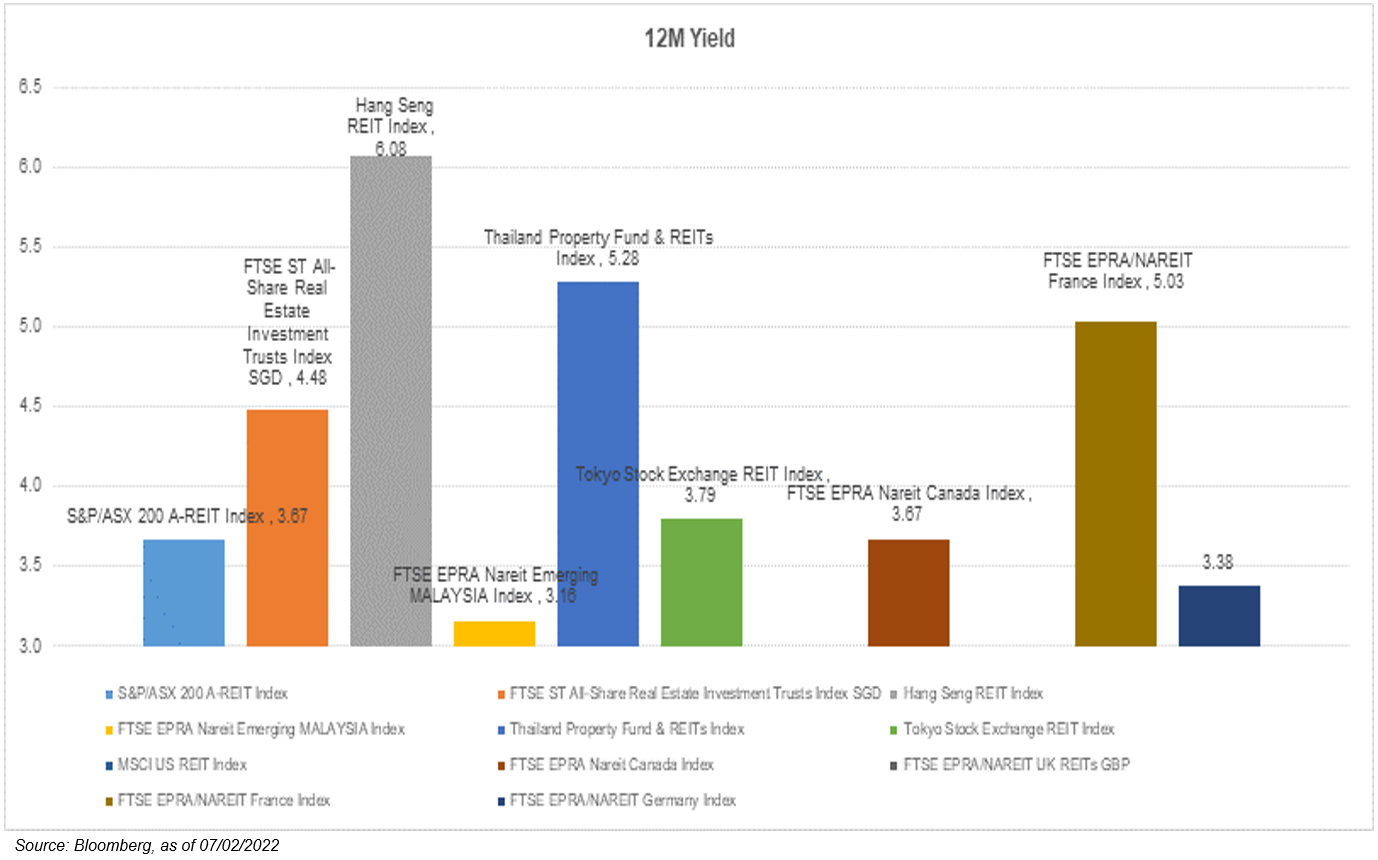

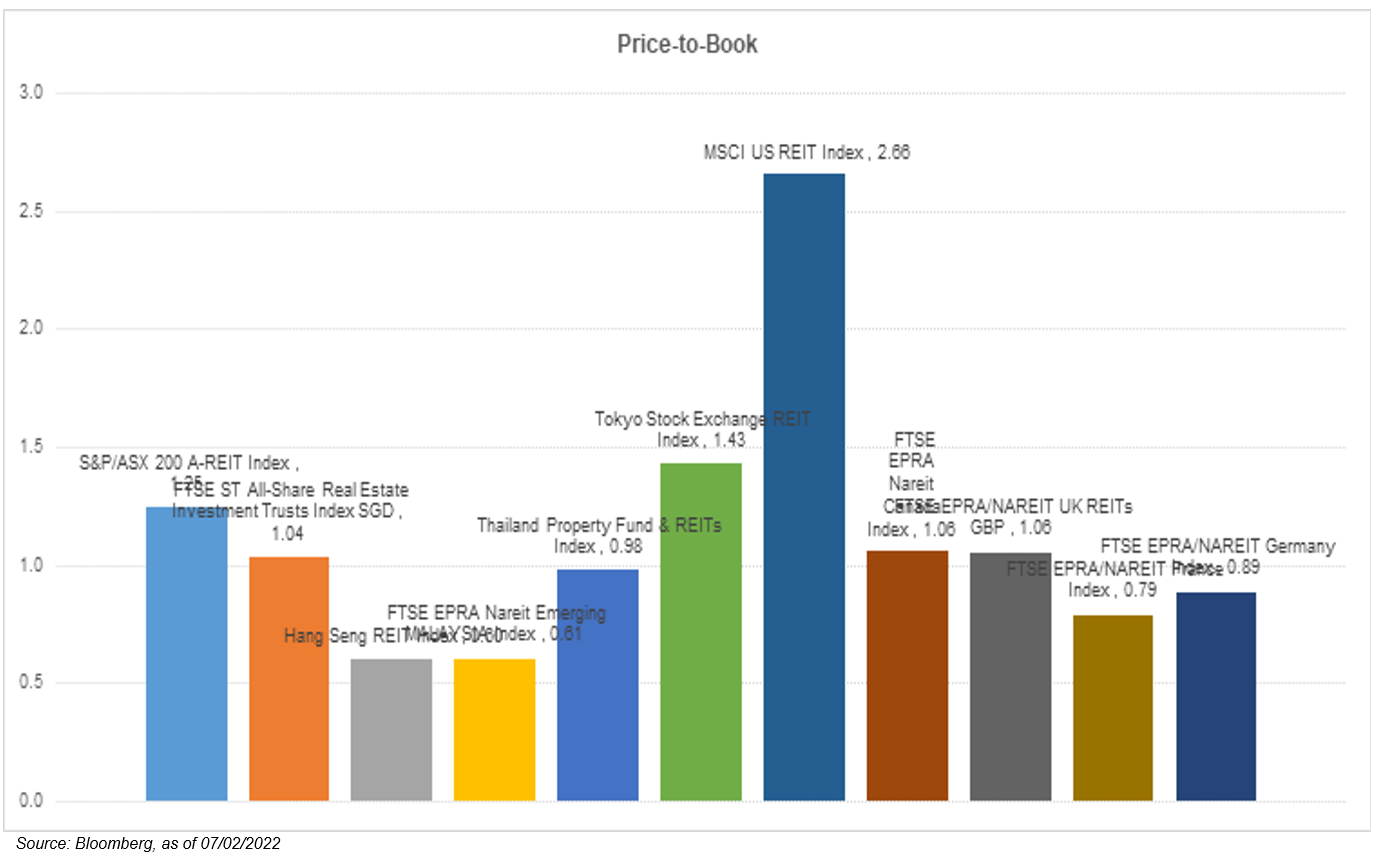

As can be seen below, the global REIT markets mostly slipped or remained flat with the exception of Australia and Singapore. However, the overall 12-month yield spreads remained positive and still favorable towards REIT’s forward total return. The iEdge S-REIT Index (+0.12%) and all the S-REIT sectors reported mostly positive returns.

As can be seen below, the global REIT markets mostly slipped or remained flat with the exception of Australia and Singapore. However, the overall 12-month yield spreads remained positive and still favorable towards REIT’s forward total return. The iEdge S-REIT Index (+0.12%) and all the S-REIT sectors reported mostly positive returns.

Back at home, we saw an uptrend in infections as the 7-day moving average of total COVID-19 cases sharply rose to 13,208 from 2,540 the previous week. Omicron had brought in a new wave of the pandemic and saw many countries tightening their restrictions to curb the spread. So far, more than 50 countries have stepped up border controls to slow the spread and Singapore had also stopped all new vaccinated travel lanes (VTLs) destinations until 20th January. The VTLs launch with Qatar, Saudi Arabia and the United Arab Emirates are currently deferred until further notice. Virus development will need to be closely observed in order to identify the right time for a recovery play as the Omicron will likely delay the pace moving forward.

Important Information

This material is provided by Phillip Capital Management (S) Ltd (“PCM”) for general information only and does not constitute a recommendation, an offer to sell, or a solicitation of any offer to invest in any of the exchange-traded fund (“ETF”) or the unit trust (“Products”) mentioned herein. It does not have any regard to your specific investment objectives, financial situation and any of your particular needs. You should read the Prospectus and the accompanying Product Highlights Sheet (“PHS”) for key features, key risks and other important information of the Products and obtain advice from a financial adviser (“FA“) before making a commitment to invest in the Products. In the event that you choose not to obtain advice from a FA, you should assess whether the Products are suitable for you before proceeding to invest. A copy of the Prospectus and PHS are available from PCM, any of its Participating Dealers (“PDs“) for the ETF, or any of its authorised distributors for the unit trust managed by PCM.

An ETF is not like a typical unit trust as the units of the ETF (the “Units“) are to be listed and traded like any share on the Singapore Exchange Securities Trading Limited (“SGX-ST”). Listing on the SGX-ST does not guarantee a liquid market for the Units which may be traded at prices above or below its NAV or may be suspended or delisted. Investors may buy or sell the Units on SGX-ST when it is listed. Investors cannot create or redeem Units directly with PCM and have no rights to request PCM to redeem or purchase their Units. Creation and redemption of Units are through PDs if investors are clients of the PDs, who have no obligation to agree to create or redeem Units on behalf of any investor and may impose terms and conditions in connection with such creation or redemption orders. Please refer to the Prospectus of the ETF for more details.

Investments are subject to investment risks including the possible loss of the principal amount invested, and are not obligations of, deposits in, guaranteed or insured by PCM or any of its subsidiaries, associates, affiliates or PDs. The value of the units and the income accruing to the units may fall or rise. Past performance is not necessarily indicative of the future or likely performance of the Products. There can be no assurance that investment objectives will be achieved. Any use of financial derivative instruments will be for hedging and/or for efficient portfolio management. PCM reserves the discretion to determine if currency exposure should be hedged actively, passively or not at all, in the best interest of the Products. The regular dividend distributions, out of either income and/or capital, are not guaranteed and subject to PCM’s discretion. Past payout yields and payments do not represent future payout yields and payments. Such dividend distributions will reduce the available capital for reinvestment and may result in an immediate decrease in the net asset value (“NAV”) of the Products. Please refer to <www.phillipfunds.com> for more information in relation to the dividend distributions.

The information provided herein may be obtained or compiled from public and/or third party sources that PCM has no reason to believe are unreliable. Any opinion or view herein is an expression of belief of the individual author or the indicated source (as applicable) only. PCM makes no representation or warranty that such information is accurate, complete, verified or should be relied upon as such. The information does not constitute, and should not be used as a substitute for tax, legal or investment advice.

The information herein are not for any person in any jurisdiction or country where such distribution or availability for use would contravene any applicable law or regulation or would subject PCM to any registration or licensing requirement in such jurisdiction or country. The Products is not offered to U.S. Persons. PhillipCapital Group of Companies, including PCM, their affiliates and/or their officers, directors and/or employees may own or have positions in the Products. This advertisement has not been reviewed by the Monetary Authority of Singapore.